info@encore-funding.com

info@encore-funding.com 216-998-9900

216-998-9900

Invoice Funding Fees: How Much Does It Cost?

When I talk with staffing entrepreneurs about invoice funding, they inevitably say, “This sounds great, but how much will it cost?” It’s a fair question. Because invoice funding is a flexible financial tool, the fees can vary.

Read on to uncover how much invoice funding costs and the extra benefits it offers compared to traditional financing.

How to Know What Your Invoice Funding Fees May Be

The short answer is: it depends! I know, it’s a bit of a general answer, but it does depend on which invoice funding fee we’re talking about: discount fee or service fee.

Discount fees are the main cost associated with invoice funding. They’re calculated as a percentage of the total value of your invoices, usually 1-3%. The discount fee is typically determined by a variety of factors such as the number and size of your invoices, the time it takes for customers to pay you and the creditworthiness of your customers.

Service fees are typically less than the discount fee. Service fees cover administrative costs associated with setting up and tracking invoices, monitoring customer payments, invoice collection and other services.

On top of discount and service fees, it’s common for factors to charge you an up-front fee for invoice funding services. At Encore Funding, that’s not our style. We keep it simple and cost effective for you to factor invoices and keep cash flowing through your staffing business.

Because factors focus their credit decisions almost solely on your accounts receivable, you can understand your rates and receive funds much quicker than you would with traditional bank financing.

What Influences Invoice Funding Fees?

Just like other funding partners, we consider several business aspects to determine your invoice funding fees. These are the most common.

- Strength of your customers’ credit: A major benefit of invoice funding vs. traditional financing is that factors consider your customers’ credit, not yours. The better your customers’ credit, the less risk they present to a factor, the lower your invoice funding fee!

- Number of customers invoiced: We’re interested in the number of clients you do business with. More clients on your roster spreads the risk out, which can lower your funding fees. On the other hand, a larger number of clients may increase your service fees.

- Funding-only vs. Full-service funding: Most funders offer two main kinds of services: funding only or full service. Full-service funding increases your fees because there are added benefits like client credit monitoring, invoicing, payroll processing, payroll tax preparation and filing, W-2s and more. Learn more about our solutions for both services here.

- Payment terms for your customers: It’s critical to be on a consistent invoice schedule with your customers. If a factor observes that invoices are typically unpaid for a long time, it may increase your fees because the risk increases the longer invoices are outstanding.

Invoice Funding vs. A Bank Loan

So, we’ve covered the two main types of invoice funding fees and what influences them. Now, onto another hot topic: what’s the cost difference between invoice funding and a bank loan?

While a bank loan can offer your staffing business some much-needed cash, it usually comes with time-consuming paperwork, administrative tasks and strict requirements.

With invoice funding, you get funds upfront without a lengthy bank approval process. Plus, invoice funding is considered off-balance sheet debt, so it won’t show up on your financials.

Also, factors heavily focus credit decisions on the strength of your customers rather than the strength of your balance sheet. Let’s use a relatively new staffing company as an example. Banks will most likely turn a staffing entrepreneur down for a loan because the balance sheet doesn’t meet their strict requirements. However, if the staffing company’s customers are creditworthy, they will have a tremendous amount of liquidity available to them with a factor.

Although a bank loan is usually less expensive, the benefits of partnering with a trusted funding partner like Encore Funding will support your long-term growth more. By nature, banks discourage their clients from growing quickly because of strict regulations.

We flip that, because we’re committed to your success. A funding partner not only embraces client growth but can also provide the additional financing needed to fuel it.

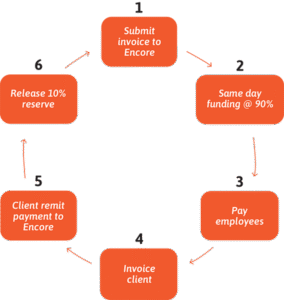

Here’s a quick view into how this works. When you use payroll funding, the funder (Encore) advances up to 90% of the invoice while you wait for payment. Once your clients pay their invoice, we complete the transaction by depositing the remaining balance, minus a small fee, into your bank account.

The Application & Approval

During the funding application process, new staffing entrepreneurs often think poor personal or business credit means they can’t access funding. Not true! As I mentioned above, your customers’ credit histories are much more important to a factor.

Another myth is that an invoice funding application is lengthy. Again, this isn’t the case. At Encore Funding, it’s a simple process that takes ten to twelve business days from start to finish. Here are the requirements for invoice funding application and approval at Encore Funding:

- Completed Application: One to two pages that share more information about your business so we can get to know you.

- Articles of Incorporation: This is simply to verify that your business exists!

- A current accounts receivable aging report: It’s important for us to know how long it takes for your customers to pay you.

- Customer list: We verify who you do business with to run a credit report on each customer (your customers won’t know their credit was checked).

- Proof of Workers Compensation Insurance: This is to ensure you have the right coverage for your business.

- Copies of customer contracts: It’s important for us to make sure you have a binding legal relationship with each of your customers.

Is Invoice Funding Right for You?

It’s best practice to evaluate all financing options available to you. Funding, bank financing, and asset-based lending each have their own benefits, but funding is often the best option for staffing firms. We’re happy to talk through your situation with you to understand which path makes sense to explore.

A trusted funding partner provides easy access to working capital without the hassle of complex paperwork and approval processes. Plus, invoice funding focuses on your customers’ creditworthiness rather than your business’s balance sheet.

I’m proud to be part of a team that’s made of entrepreneurs serving entrepreneurs. Our passion is to help you grow! Apply here and one of our team members will be in touch to discuss your customized fee structure.

Associations and Affiliations

")

")